Join the Quant Scientist Newsletter

Gain access to exclusive tools that Wall Street's Elite don't want you to have. Don't miss the next issue...

Join 11,500+ Quant Scientists learning one article at a time

Join 11,500+ Quant Scientists learning one article at a time

How to make an Algorithmic Trading Strategies using Machine Learning Prediction with Python

We're working on the second Cohort of the Python for Algorithmic Trading course, and Jason and I are expanding the curriculum into Machine Learning and Data Science. And, we want to fill you in on some powerful algorithmic trading strategies we are exploring. Machine Learning is one of them (inspired by a Twitter post, story inside). We'll cover how to use Machine Learning for locating long and short positions automatically.

This article serves as an introduction to Machine Learning for Algorithmic Trading. We cover:

Why Machine Learning for Algorithmic Trading?

Full Python Tutorial: Algorithmic Trading with Machine Learning using Python

BONUS: Get the Python Code for EVERYTHING you see in this post

Disclaimer:

The information and educational material provided by Quant Science, LLC are for educational purposes only and should not be considered as financial advice or recommendations to purchase, hold, or sell any securities or other financial instruments. Before you proceed, please review our full disclaimer here.

Quick favor - We're preparing for Cohort 2 of our new algorithmic trading course. If you can spare 60 seconds, we'd love to hear what you want out of the course. Click here to enter your 60-second survey.

Join the Quant Scientist Newsletter (and Get the Code)

Want exclusive access to our FULL codebase for this Quant Science tutorial plus dozens more? The code is in the QS007 Folder. Join here:

Why Machine Learning for Algorithmic Trading?

Machine learning in the context of algorithmic trading can be crucial for detecting patterns that indicate long and short positions, which we'll cover in this tutorial.

Analysis from Danny Groves (@DrDanobi)

This introductory analysis shows the power of machine learning for a simple trend prediction using Machine Learning. Here's the original Twitter post from Danny.

Machine Learning for Indicating Potential Long/Short Regions

Danny's goal was to predict regions where the stock is expected to be above the Target (20-Day Simple Moving Average) over the next 5 Days. We can use this information for identifying Long/Short positions in assets such as the SPY.

Ok, let's dive into a python tutorial.

Python Tutorial: How to make an Algorithmic Trading Strategy using Machine Learning

The goal with our analysis is to set up a framework for a simple trend prediction on the SPY (the ETF that tracks the S&P 500 index). We'll examine how we can produce trends that indicate regions of potential long and short positions. Get the code: It's in the QS007 folder.

Step 1: Load Libraries and Set Up the Analysis Parameters

The first step in our analysis is to load the following libraries and setup our analysis parameters. Run this code:

Get the code: It's in the QS007 folder.

Step 2: Import and Visualize the Data

Next, let's import data on the "SPY", which is the ETF that tracks the S&P 500 index. We can visualize its close price over the time period being analyzed. Run this code:

Get the code: It's in the QS007 folder.

This returns an interactive plot showing the SPY closing price for the time period specified in the analysis setup.

Step 3: Feature Engineering

Machine Learning algorithms like Random Forest need features to help it model the system and make predictions. To do so, we can use these features from Danny's original analysis.

Distance from N-Day Moving Average Features

Distance from N-Day High/Low Rolling Features

Price Distance from N-Day Lag

Run this code:

Get the code: It's in the QS007 folder.

This adds 19 new features (columns) to our original data.

Step 4: Create the Target Variable

In Machine Learning, a target variable is what the machine learning model uses to predict. In our case, we need to create this feature.

First make a 20-day simple moving average.

Then determine True/False if the Closing price is greater than the 20-day simple moving average.

Finally, create a 5-day lead (negative lag) to determine if the price 5-days ahead will be above the moving average.

Run this code:

Get the code: It's in the QS007 folder.

This adds the features needed to predict probability of the close price being above the SMA in the next 5 days.

Step 5: Clean and Train/Test Split

Next, let's clean up our data and produce the train/test splits, which will be used by our machine learning model to train and evaluate performance. Run this code:

Get the code: It's in the QS007 folder.

Step 6: Train the Random Forest Model

Now we're ready for the fun part: training the machine learning model. This model will be used to predict whether or not the closing price will be above or below the 20-day SMA in the next 5 days. Run this code to train the Random Forest Classifier:

Get the code: It's in the QS007 folder.

This produces both in-sample (training) and out-of-sample (testing) accuracy and precision metrics:

An out-of-sample AUC of 0.79 is better than random guessing, indicating this could be a profitable strategy. However, it's essential to backtest and use a paper trading account prior to going live. We teach how to do this in our python algorithmic trading course.

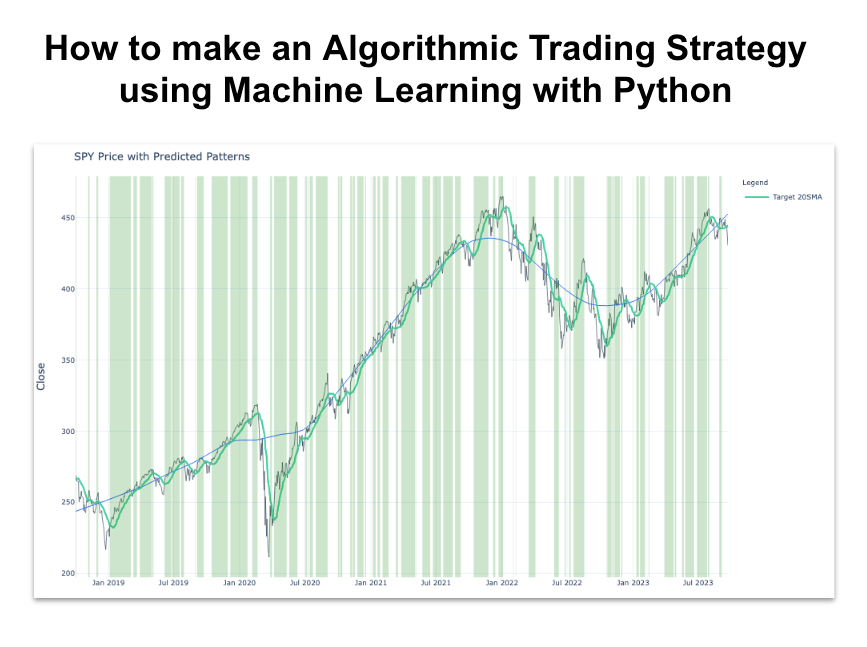

Step 7: Visualize the Predicted Regions for 5-Day Lead of Close > 20-Day SMA

The last step for this tutorial is to plot the Predicted Regions where the 5-Day Lead of Close is greater than the 20-Day SMA. The code for this visualization is extensive, and you can join our newsletter to get it. The plot code is in the QS007 folder.

Get the code: It's in the QS007 folder.

Conclusion: Python is getting even better for Stock Analysis

By now you can tell that we are giving you every POSSIBLE tool and skill to enhance your Algorithmic Trading game.

Ready to take your investment game to the next level? Embracing Python for algorithmic trading can be a game-changer for your portfolio. If you're new to Python or want to sharpen your skills for financial analysis, our upcoming Python for Algorithmic Trading Course is the perfect opportunity. See you in our Python Algo-Trading course!

Are you feeling lost when trying to learn Algorithmic Trading?

There's nothing worse than going at this alone--

❌ Learning Python is tough.

❌ Learning Trading is tough.

❌ Learning Math & Stats is tough.

It's no wonder why it's easy to feel lost.

And all of this increases the likelihood you will fail (not to mention lose money in the process). Protect your future.

👉 Join 3600+ future Quant Scientists on our Python for Algorithmic Trading Course Waitlist: https://learn.quantscience.io/python-algorithmic-trading-course-waitlist

Start Your Journey To Becoming A Quant Today!

Join the Quant Scientist Newsletter

Gain access to exclusive tools that Wall Street's Elite don't want you to have. Don't miss the next issue...

Join 11,500+ Quant Scientists learning one article at a time

Join 11,500+ Quant Scientists learning one article at a time