Join the Quant Scientist Newsletter

Gain access to exclusive tools that Wall Street's Elite don't want you to have. Don't miss the next issue...

Join 11,500+ Quant Scientists learning one article at a time

Join 11,500+ Quant Scientists learning one article at a time

Portfolio Optimization with Riskfolio-Lib (Top 9 Functions)

Python is wild for finance! Case in point: Portfolio optimization with Riskfolio-Lib. In this QS Newsletter (get the code), we are sharing some of the insane functionality you get inside this awesome Python package, Riskfolio-lib. Today, you learn:

What Riskfolio-Lib is (and why it's important for Portfolio Optimization)

The 9 best portfolio optimization functions inside riskfolio-lib

BONUS: Get the Python Code for EVERYTHING you see in this post

Disclaimer:

The information and educational material provided by Quant Science, LLC are for educational purposes only and should not be considered as financial advice or recommendations to purchase, hold, or sell any securities or other financial instruments. Before you proceed, please review our full disclaimer here.

Join the Quant Scientist Newsletter (and Get the Code)

Want exclusive access to our FULL codebase for this Quant Science tutorial plus dozens more? The code is in the QS0014 Folder. Join here:

NEW: Free 5-Day Algorithmic Trading Course.

Are you interested in learning Algorithmic Trading with Python? Do you want to learn how to execute trades automatically, how to find edge, backtest trading strategies, analyze risk, then take your winning trades from Paper Account to Production (Live Trading)?

If the answer is Yes, then we have a NEW Free 5-Day Algorithmic Trading.

Click here to join our free 5-Day Algorithmic Trading Course.

What is Riskfolio-Lib (and why is it important for Portfolio Optimization)?

Riskfolio-Lib is a Python library designed for making portfolio optimization easier and more accessible. It offers a comprehensive suite of tools that allow users to construct, analyze, and optimize portfolios based on different strategies and risk measures. This library stands out because it focuses not only on traditional mean-variance optimization but also incorporates more advanced visualizations and portfolio analysis.

Key Features of Riskfolio-Lib

Risk Measures: Riskfolio-Lib allows portfolio optimization using various risk measures including Variance, Standard Deviation, Semi-Standard Deviation, VaR, CVaR, Maximum Drawdown, and others. This flexibility is particularly useful for users who want to tailor their risk assessment to specific investment philosophies or regulatory requirements.

Optimization Models: The library supports different optimization models like Markowitz’s classical mean-variance model, risk parity models (where the risk contribution of all portfolio components is equalized), and maximum diversification strategies.

Asset Allocation: It offers tools to perform asset and factor allocation, which are crucial for constructing a balanced portfolio that aligns with the investor's risk tolerance and investment goals.

Constrained Optimization: Users can add constraints to the optimization problem, such as setting minimum and maximum weights for assets, which is important for practical portfolio implementation considering transaction costs, liquidity issues, and regulatory restrictions.

Performance Analysis: Riskfolio-Lib can generate various plots and visualizations to analyze the performance and risk of portfolios, making it easier to compare different portfolio configurations and their adherence to a chosen risk profile.

Integrated Solution: It integrates with other Python libraries like

pandasfor data manipulation,numpyfor numerical operations, and plotting libraries such asmatplotlibandseaborn, offering a cohesive environment for portfolio analysis.

Importance of Riskfolio-Lib for Portfolio Optimization

Risk-Focused Investing: Traditional portfolio optimization often focuses mainly on the returns, using the variance as a measure of risk. Riskfolio-Lib's ability to use various and more complex risk measures allows for more sophisticated risk management strategies, which are particularly valuable in volatile or uncertain market conditions.

Customization and Flexibility: Investors and financial analysts can create highly customized investment strategies that meet specific risk-return profiles, which is crucial for achieving diversified investment goals.

Practical Application and Compliance: The ability to incorporate various constraints helps ensure that the optimized portfolios are not only theoretically optimal but also practical and compliant with real-world investment constraints.

Educational and Research Tool: For students and researchers in finance, Riskfolio-Lib offers a powerful tool to explore advanced portfolio theories and conduct empirical research in asset pricing and portfolio management.

The 9 Best Portfolio Optimization Functions Inside Riskfolio-Lib

Ok, let's dive in and see what you can do with Riskfolio-Lib. First, make sure to sign up for our Newsletter to get all of the code you see today.

Next, run this code from the "QS014-Riskfolio" Folder:

This code downloads the stock assets and coverts to returns.

#1. Portfolio Objects

The #1 most important part of Riskfolio-Lib is understanding how to set up Portfolio Objects. Run this code to create the Portfolio Object:

#2. Optimizing for Max Sharpe (Max Risk Adjusted Return Ratio)

The #2 most important part of Riskfolio that you need to know is how to optimize the portfolio. Here we do a simple optimization for max Sharpe ratio. Run this code:

#3. Efficient Frontier Portfolios

The #3 most important part of Riskfolio is using it to estimate high returns portfolios along the efficient frontier. Run this code to make 20 optimized portfolios:

#4. Cumulative Returns Plot

The #4 most important part is getting cumulative returns plot. It's super simple. Just run this code:

#5. Efficient Frontier Plot

The #5 most important function is the Efficient Frontier Plot. Run this code:

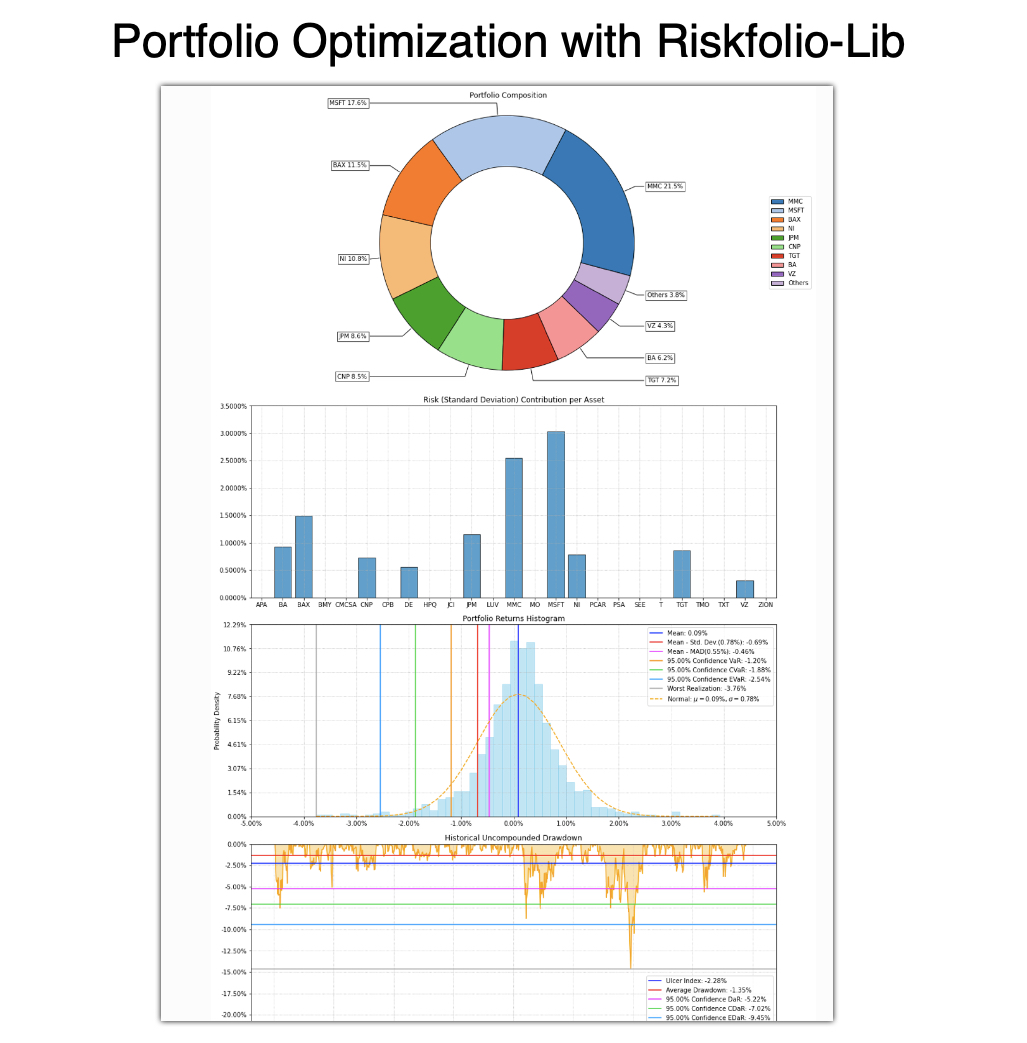

#6. Portfolio Donut Chart

At number #6, we have the portfolio donut chart. Run this code:

#7. Plot Table (Risk Metrics)

At Number #7, we have Plot Table for getting risk metrics. Run this code:

#8. Plot Risk Contribution

At number #8, we have the risk contribution plotting capabilities of Riskfolio-Lib. Run this code:

#9. Excel Report

And rounding out our top 9 most important functions from Riskfolio-Lib is none other than it's Excel Report utility. Get all of your portfolio optimization analysis straight to Excel. Just run this code:

Conclusion: Riskfolio-Lib for Portfolio Optimization

Python is wild for finance. It's hard to believe these tools are available for free. Riskfolio-lib is insane for portfolio optimization.

But having access to the tools doesn't guarantee results. You still need to:

Generate trading strategies

Backtest strategies

Execute trades

You can go at it alone. Or you can learn with 200+ of us that are learning to apply python to algorithmic trading to grow investments.

Ready to make Algorithmic Trading Strategies that actually work?

There's nothing worse than going at this alone--

❌ Learning Python is tough.

❌ Learning Trading is tough.

❌ Learning Math & Stats is tough.

It's no wonder why it's easy to feel lost, make bad decisions, and lose money.

Want help?

👉 Join 7,900+ future Quant Scientists on our Python for Algorithmic Trading Course Waitlist: https://learn.quantscience.io/python-algorithmic-trading-course-waitlist

Start Your Journey To Becoming A Quant Today!

Join the Quant Scientist Newsletter

Gain access to exclusive tools that Wall Street's Elite don't want you to have. Don't miss the next issue...

Join 11,500+ Quant Scientists learning one article at a time

Join 11,500+ Quant Scientists learning one article at a time